B

Bad Credit

A poor credit score as measured by the credit reporting agencies. Bad

Credit is caused by making late payments, missing payments, exceeding

card limits or filing for bankruptcy. Steps can, and should be taken to

repair bad credit. Balance

The outstanding amount owed to a creditor on a particular account.

Balance Transfer

The transfer of one or more credit card balances onto another card,

typically to take advantage of a lower annual percentage rate.

Balloon Payments

A loan with a balloon payment requires that a single, lump-sum payment

be made at the end of the loan.

Bankruptcy

A declaration of the inability to make debt payments under the current

agreed upon terms. Once a bankruptcy has been filed, foreclosures, garnishments,

repossessions, utility cut-offs and debt collection activities are automatically

stayed. Consumers can file Chapter 7 or Chapter 11 bankruptcy.

Bankruptcy Code

The federal laws governing the conditions under which people can declare

bankruptcy and the procedures under which persons claiming inability

to repay their debts can seek relief.

C

Capacity

Factor in determining creditworthiness by comparing a borrower’s

income and the amount of debt the borrower carries at the time the application

for credit is made. While capacity may be considered in a credit decision,

a credit report does not contain information about earning ability or

the likelihood of continuing income.

Chapter 7 Bankruptcy

Chapter of the Bankruptcy Code that provides for court administered

liquidation of the assets of a financially troubled individual or business.

Chapter 11 Bankruptcy

Chapter of the Bankruptcy Code that is usually used for the reorganization

of a financially troubled business. Used as an alternative to liquidation

under Chapter 7. The U.S. Supreme Court has held that an individual

may also use Chapter 11. Terms of contracts can be renegotiated under

Chapter 11.

Chapter 12 Bankruptcy

Chapter of the Bankruptcy Code adopted to address the financial crisis

of the nation’s farming community. Cases under this chapter are

administered like Chapter 11 cases, but with special protections to

meet the special conditions of family farm operations.

Chapter 13 Bankruptcy

Chapter of the Bankruptcy Code in which debtors repay debts according

to a plan accepted by the debtor, the creditors and the court. Plan

payments usually come from the debtor’s future income and are

paid to creditors through the court system and the bankruptcy trustee.

Charge Card

A form of credit card that requires full payment of the balance each

month. Such cards nevertheless appear on your credit report, since they

do extend credit to you, even though it is for only a short amount of

time. Examples include American Express or Diners Club cards.

Charge-Off

Action of transferring accounts deemed uncollectible to a category such

as bad debt or loss. Collectors will usually continue to solicit payments,

but the accounts are no longer considered part of a company’s

receivable or profit picture. This is used when an instance in which

a consumer is seriously delinquent in with payments and the creditor

elects to transfer the account to an accounting category that reflects

the debt as a loss on the creditor’s accounting books. Charge-Off

accounts are typically sent to a collection agency and are reported

to the major credit reporting agencies.

Civil Action

Any court action against a consumer or business in order to obtain money

they feel the defendant owes them. Examples include a wage assignment,

child support judgment, small claims judgment or a civil judgment.

Claim Amount

The amount awarded in a court action.

Closed Date

The date an account was closed.

Closing Costs

Expenses that buyers incur in the transfer of ownership of a property.

Closing costs may include taxes, origination fees, attorney's fees,

and other costs.

Co-maker

A creditworthy co-maker is sometimes required in situations where an

applicant’s qualifications are marginal. A co-maker is legally

responsible to repay the charges in the joint account agreement.

Consumer

An individual who purchases products and services.

Consumer Debt

Debt incurred for items that aren't considered tangible investments

such as credit card debt, car loans, and personal loans.

Co-signer

A person who pledges in writing, as part of a credit contract, to repay

the debt if the borrower fails to pay the debt in full. The account

displays on both the borrower’s and the co-signers credit reports.

Credit

The borrowing capacity of an individual or company, typicaly based on

their ability and history of repaying loans.

Credit Agency

See Credit Bureau.

Credit Bureau

Commonly known as credit bureaus or credit reporting agencies, credit

bureaus are companies that receive, maintain, and provide information

about consumers' credit history. The three major agencies are Equifax,

Experian, and TransUnion. There are also many smaller agencies; however,

most of them get information from one or more of the three major agencies.

Credit Card

A card used to make purchases or take out cash loans that require the

user to pay some or the entire outstanding amount each month. Credit

cards are differentiated mainly by their terms.

Credit History

A record of how a consumer has (or has not) made payments on credit

accounts in the past. An individual’s credit history is considered

to be the best guide in determining whether or not the consumer is likely

to pay future payments on time.

Credit Limit

The maximum amount a borrower can draw upon or the maximum that an account

can show as outstanding for a particular line of credit.

Credit Items

Information reported by current or past creditors found on credit reports.

Credit scores are calculated based on credit items.

Credit Report

A report on a consumer’s payment history as reported by their

creditors to the major consumer credit reporting agencies. The agencies

provide this information to credit grantors who have a permissible purpose

under the law to review the report.

Credit Risk

The likelihood of a consumer to pay back an outstanding debt on time

or in full.

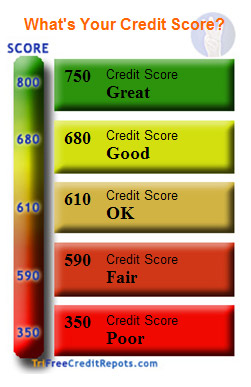

Credit Score

A numerical estimation of the likelihood that you'll meet debt obligations

used by credit grantors to provide an objective means of determining

risks in granting credit. Credit scoring increases efficiency and timely

response in the credit granting process. Credit scores are based on

a consumers credit history and range from 300 to 800.

Creditor

A company or individual that enables consumers to make purchases on

credit and/or lends consumers money. Sometimes used interchangeably

with lender.

Creditworthiness

The ability of a consumer to receive favorable consideration and approval

for the use of credit from an establishment to which they applied.

D

Daily Periodic Rate

A credit card's annual percentage rate divided by 365 days.

Debt-to-Income Ratio

An individual or companies income compared to their debt owed.

Delinquent

Accounts classified into categories according to the amount of time

a payment is past due. Common classifications are 30, 60, 90 and 120

days past due. Special classifications also include charge-off, repossession,

transferred, etc.

Discharge

A judgment that may be granted by the court to release a debtor from

most of his debts that was included in a bankruptcy. Some debts cannot

be included in the bankruptcy and cannot be discharged. Examples include

alimony, taxes, child support, and liability for willful and malicious

conduct and certain student loans.

Dismissed (Bankruptcy)

When a consumer files a bankruptcy, the court may decide to not allow

the consumer to continue with the bankruptcy. If the judge rules against

the petition, the bankruptcy is known as dismissed.

Dispute (Disputing

items on credit reports)

If a consumer believes an item of information on their credit report

is inaccurate or incomplete, they may challenge, or dispute the item.

The credit agencies will investigate and correct or remove any inaccurate

information or information that cannot be verified. Consumers have the

option of disputing issues online or they may call the telephone number

located on their credit report s for assistance.

E

ECOA

Standard abbreviation for Equal Credit Opportunity Act. (See Equal Credit

Opportunity Act below.)

End-user

A business that receives the report for decision making purposes that

meet the permissible purpose requirements of the FCRA.

Equal Credit Opportunity Act (ECOA)

Federal law, which prohibits creditors from discriminating against credit

applicants on the basis of sex, marital status, race, color, religion,

age, and/or receipt of public assistance.

Equifax

One of the three national credit reporting agencies or bureaus. The

other two are Experian and TransUnion.

Experian

One of the three national credit reporting agencies or bureaus. The

other two are Equifax and TransUnion.

F

Fair Credit and Charge Card Disclosure Act (1971; amended in 1997 and

2003)

Amendments to the Truth In Lending Act that require the disclosure of

the costs involved in credit card plans that are offered by mail, telephone

or applications distributed to the general public.

Fair Credit Billing

Act

Federal legislation that provides a specific error resolution procedure

to protect credit card customers from making payments on inaccurate

billings.

Fair Credit Reporting

Act (FCRA)

Federal legislation governing the actions of credit reporting agencies.

Fair Debt Collection

Practices Act (FDCPA)

Federal legislation prohibiting abusive and unfair debt collection practices.

Finance Charge

The amount of interest you will be required to pay. Finance charges

are usually included in the monthly payment total.

Fixed Rate

An annual percentage rate (APR) that does not change, meaning that the

interest rates do not fluctuate over the life of the loan.

Foreclosure

The legal process by which a creditor may sell mortgaged property to

recover a defaulted mortgage.

Fraud Alert

If you suspect that you're the victim of identity theft or credit fraud,

you may contact the credit reporting agencies and place a fraud alert

on your credit file. Such an alert will prevent new credit accounts

from being opened without your express permission.

G

Garnishment

A legal process whereby a creditor has obtained a judgment on a debt

that allows him to receive full or partial payment by seizure of a portion

of the debtor's assets (wages, bank account, etc.).

Grace Period

The time period you have to pay a bill in full and avoid interest charges.

Generation Identifier

Generation identifiers. Examples include Jr., Sr., II, III and IV.

Gross Monthly Income

What you earn each month before taxes are deducted.

Guarantor

Person responsible for paying a balance.

H

Hard Inquiry

An indication on your credit report that a lender has obtained a copy

of the report in order to evaluate your creditworthiness for a loan

or credit line. An excessive amount of hard inquiries within a six-month

period may lower your credit score; this allows individuals time to

shop around for large purchases such as homes. All the inquiries consumers

make concerning their credit reports and scores are considered soft

inquiries and never affect their credit score.

High Balance

The highest amount that you have owed on an account.

Home Equity

The part of your home you actually own, or the home's current market

value minus the amount you still owe.

Home Equity Loan

A loan secured by using a primary residence or second home as collateral

to the extent of the excess of fair market value over the debt incurred

in the purchase. Interest on a home equity loan may be tax deductible,

but if you fail to pay your home equity loan, your home could be sold

to pay off the debt (foreclosure).

I

Identity Theft

A growing and alarming area in crime that happens when someone uses

your personal information to fraudulently obtain and use your credit.

Credit monitoring and protection is an effective means to detect and

deter identity theft.

Installment Credit

Credit accounts in which the debt is divided into amounts to be paid

successively at specific intervals.

Investigation

The process a consumer credit reporting bureau goes through in order

to verify or correct credit report information that is disputed. The

credit grantor who supplied the information is contacted and asked to

review the information. The creditor will then tell the credit reporting

bureau if the information is accurate as it appears, or they will give

the corrected information to update the credit report.

Interest Rate

The amount charged by a lender over time for borrowing money.

Involuntary Bankruptcy

A petition can be filed by certain credit ors to have a debtor judged

bankrupt. If the bankruptcy is granted, it is referred to as an involuntary

bankruptcy.

J

Judgment Granted

The final determination of a court upon matters submitted to it regarding

the rights and obligations of the parties involved in the lawsuit.

L

Last Reported

The date on a credit report that the creditor last reported information

about the account.

Liability amount

Amount for which a creditor is legally obligated.

Lien

A legal document used to create a security interest in another’s

property. A lien is frequently given as a security for the payment of

a debt and means that the consumer’s property is being used as

collateral during repayment of the money that is owed. Liens can be

placed against a consumer for failure to pay money owed to cities, counties,

states or the federal government. Unpaid taxes are a common reason for

a lien to be issued.

Line of Credit

The maximum outstanding balance a borrower can draw upon for an account.

M

Mortgage Identification Number (MIN)

This number indicates that a loan is registered with Mortgage Electronic

Registration Systems Inc., which tracks the ownership of mortgages.

It will be used to permanently identify a mortgage.

Most Recent Date

The date of the most recent account balance was provided.

N

Notice of Results

When investigations produce changes in credit reports you may request

that credit agencies send the corrected information in your credit history

to eligible credit grantors and employers who reviewed your information

within a specific period of time.

O

Obsolescence

This is how long negative information will stay in a credit report before

it’s not relevant to the credit granting decision. The obsolescence

period is 10 years for bankruptcy and 7 years in all other instances.

However, unpaid tax liens may remain indefinitely, although Experian

removes them after 15 years.

Original Amount

The amount owed to a creditor before interest was incurred.

P

Payment Status

The history of an account, including any delinquencies or derogatory

conditions occurring during the previous seven years. Examples include:

Current, delinquent 30, current was 60, redeemed repossession and charge-off

)

Permissible Purposes

This occurs when a credit report is issued to a third party. Some permissible

purposes are credit transactions, insurance underwriting, court orders,

subpoenas, and written instructions of the consumer.

Personal Statement

A request that a general explanation about the information on your report

be added to your report. This statement remains for two years and displays

to anyone who reviews your credit information.

Potentially Negative

Items

Any potentially negative credit items, judicial rulings or public records

that could possibly have an effect on your creditworthiness.

R

Recent Balance

The most recent reported balance owed on a credit account.

Recent Payment

The most recent reported amount paid on an account.

Released

This means that a lien has been satisfied and no longer applies.

Reported Since

The date the creditor started reporting the account to the credit bureaus.

Repossession

When a borrower has fallen significantly behind in payments and the

creditor retakes possession of pledged.

Request an Investigation

An investigation can be applied for if information on your report is

inaccurate. The credit reporting bureaus will then contact the sources

of the information to check their records at no cost. Incorrect information

will be corrected and any information that cannot be verified will be

deleted.

Request of Credit

History

When a creditor, direct marketer or potential employer makes a request

for information from a consumer’s credit report, an inquiry is

shown on the report. Potential creditors only see credit inquiries generated

by other creditors as a result of an application of some kind. Consumers

see all listed inquiries including those by creditors, marketers and

employment inquiries. According to the Fair Credit Reporting Act, credit

grantors with a permissible purpose may inquire about your credit information

prior to your consent.

Responsibility

Indicates who is responsible for the debt of an account. Examples of

possible responsibilities are single, joint or co-signer.

Revolving Account

Credit that is automatically available up to a maximum limit so long

as a customer makes regular payments. Credit cards are an example of

revolving credit.

Risk Scoring Models

These are logarithmic calculations

A numerical determination of a consumer’s creditworthiness. Tool

used by credit grantors to predict future payment behavior of a consumer.

S

Satisfied

When the court says that a public record is paid in full by a consumer.

Secured Credit

Loan for which some form of collateral has been pledged, examples of

collateral include house or automobile.

Security

Property that a borrower pledges as collateral in the term of a loan.

Should the borrower fail to repay the loan or fall significantly behind

in payments then ownership of the property will be transferred to the

creditor following legally mandated procedures.

Security Alert

A statement that is added to a credit report by a credit agency after

it is notified that a consumer may be the victim of fraud. Security

Alerts remain on credit reports for 90 days and requires that all creditors

request proof of identification before granting credit in that person’s

name.

Service Credit

Agreements with service provider that a service will be provided to

a consumer and the consumer will pay for the services each month. Contracts

may require that payments are made for a minimum number of months, even

if the service is no longer being used. Examples common agreements of

this type are rental properties, utilities and health club memberships.

Settle

An agreement with a lender to repay only part of the original debt.

Source

The business or organization that supplied specific information on a

credit report.

Status

This indicates the current status or state of the account on a credit

report.

T

Terms

The specifics of the debt repayment schedule in a loan agreement with

a creditor. Examples include 48 months, and 60 months.

Third-Party Collectors

Collectors who collect debts for a creditor. Typically a collection

agency.

Transaction fees

Charges for the certain use of your credit line. For example, cash advance

from ATM’s frequently trigger a transaction fee.

TransUnion

One of the three national credit reporting agencies, the other two are

Experian and Equifax.

Truth in Lending Act

Title I of the Consumer Protection Act, a federal law intended to protect

borrowers from unfair lending practices. This act requires that most

lenders disclose the annual interest rate, the total cost of the loan

and other terms of loans and credit sales.

Type

This refers to the category of a credit agreement. Examples include

revolving accounts and installment loans.

U

Unsecured Credit

Also referred to as signature loans, this is when credit is extended

without collateral from the borrower. These loans are granted based

on the credit score and rarely extended to people with poor credit scores.

V

Vacated

When a judgment is rendered void.

Variable Rate

This is a loan or credit line with an annual percentage rate that changes

over time along with the prime lending rate or according to the terms

of the agreement.

Verification

This can be provided by consumers in order to make their case when they

question some information in their credit report. Credit reporting agencies

will use this documentation from the consumer when deciding what information

is correct and what will go on a disputed credit report.

Victim Statement

A statement that can be added to a credit report in order to alerts

potential credit ors that a consumer’s identification has been

used fraudulently in the past. This is a precaution to protect the consumer

who has been a victim of fraud. The statement requires that any potential

credit grantor contacts the consumer by telephone before issuing credit.

It remains in effect for seven years unless the consumer requests that

its removal.

Voluntary Bankruptcy

When a consumer files the bankruptcy on their own, as opposed to being

forced into bankruptcy by a court order.

W

Wage assignment

An agreement in which a lender is permitted to collect a certain portion

of the debtor’s wages from an employer in the event of default

on a loan.

Withdrawn

A decision to not pursue a bankruptcy or lien after court documentation

has been filed.

Writ of Replevin

A legal document issued by a court authorizing repossession of a security. |